Introduction

What are the Best Banks For Salary Account In India? If this question bothers you, then you are in right place today!

Have you ever wondered which banks offer the most rewarding salary accounts in India?

Tired of juggling multiple bank accounts and missing out on valuable perks?

Let’s face it, choosing the right “Best Bank for Salary Account in India” can feel like navigating a financial maze.

But fear not, salary warriors! My 15+ years of experience at Trupaisa.in have equipped me with the ultimate roadmap to unlock the perfect salary account fit for your needs.

Buckle up, because we’re about to dive deep into the best banks for salary account in India, their hidden benefits, and practical tips to maximize your financial well-being.

Stay tuned, and by the end, you’ll be ready to say goodbye to banking blues and hello to smarter, more rewarding finances!

Also Read: Best Neo Banks In India- A Personal Guide

Here’s what you’ll discover in this comprehensive guide:

- Top contenders: Unveil the best banks for salary account in India, carefully curated based on key factors like interest rates, fees, benefits, and customer service.

- Benefits decoded: Go beyond just “free ATM withdrawals” and explore the lesser-known perks offered by these banks, like cashback offers, insurance, and wealth management tools.

- Tailored choices: Whether you’re a tech-savvy millennial or a value-conscious professional, we’ll match you with the best bank for salary account in India that aligns with your unique financial goals and lifestyle.

- Actionable tips: Don’t just read, implement! I’ll equip you with practical strategies to leverage your salary account to its full potential, saving money and earning rewards every step of the way.

So, are you ready to transform your salary account from a mere transaction tool to a financial springboard? Let’s dive in!

What is a Salary Account?

We all have heard about a salary account, but what is it all about?

The primary purpose of a salary account is to receiving monthly salary payments from an employer.

In other words, salary account offered by banks to employees as a convenient way to receive their salaries directly into their accounts.

Salary accounts typically come with features such as no minimum balance requirements, zero or low fees, and sometimes additional benefits like higher interest rates, overdraft facilities, or discounts on loans and other financial products.

These accounts are intended for salary crediting purposes and may be converted into regular savings accounts if the account holder leaves their job or stops receiving salary payments into the account.

Also Read: 8 Best Rupay Credit Cards | Amazing Benefits | Apply Online

Why Choose a Salary Account? Features of a Salary Account

Many banks lure customers with “free ATM withdrawals,” but the true value lies in the hidden benefits that can unlock significant savings and rewards.

Let’s decode some of the lesser-known perks offered by the best banks for salary account in India:

- Cashback Offers: Earn cashback on everyday spends like bill payments, online shopping, and fuel purchases, effectively putting money back in your pocket with every transaction.

- Insurance Coverage: Enjoy complimentary accident insurance, health cover, or even travel insurance bundled with your salary account, providing peace of mind and potential savings on premiums.

- Lifestyle Discounts: Access exclusive discounts on movie tickets, dining experiences, and travel bookings, turning your salary account into a gateway to a more rewarding lifestyle.

- Wealth Management Tools: Some banks offer access to wealth management tools and investment products directly through your salary account, empowering you to take control of your financial future.

Don’t just settle for free ATM withdrawals! Explore the full range of benefits offered by different banks and choose the one that aligns with your spending habits and lifestyle goals.

Also Read: Robert Kiyosaki Financial Education | Building Wealth

How to Select the Best Salary Account in India

Choosing the “best bank for salary account in India” isn’t a one-size-fits-all solution. Your ideal bank depends on your unique financial profile and priorities. Here’s how to tailor your search:

- Tech-Savvy Millennial: If you prioritize digital convenience and seamless transactions, consider banks like Kotak Mahindra or ICICI Bank with robust mobile banking apps and innovative features.

- Value-Conscious Professional: If minimizing fees and maximizing interest rates are your top priorities, explore banks like SBI or Axis Bank with competitive interest rates and fee waivers.

- Frequent Traveler: If you travel often, prioritize banks like HDFC or Kotak Mahindra that offer airport lounge access, travel insurance, and global ATM fee waivers.

- Investment Enthusiast: If you’re looking to grow your wealth, consider banks like ICICI or Kotak Mahindra that offer access to investment products and wealth management tools directly through your salary account.

Also Read: Rupay Card Vs Mastercard: Step By Step Comparison

Top 10 Banks For Salary Account In India

Based on factors like interest rates, transaction facilities, and additional benefits, here are the top five banks for salary accounts in India:

| Bank | Interest Rate (%) | Minimum Balance Requirement | Additional Benefits |

|---|---|---|---|

| State Bank of India | 3.00 – 3.50 | None | Personalized debit card, overdraft facility, rewards program |

| HDFC Bank | 3.25 – 4.00 | Rs. 10,000 – Rs. 25,000 | Cashback on utility bills, airport lounge access, insurance |

| ICICI Bank | 3.00 – 3.75 | None | Lifestyle discounts, reward points, complimentary insurance |

| Axis Bank | 3.50 – 4.25 | Rs. 10,000 – Rs. 25,000 | Fuel surcharge waiver, dining discounts, airport lounge access |

| Kotak Mahindra Bank | 3.25 – 3.75 | Rs. 10,000 – Rs. 20,000 | Cashback on online shopping, movie tickets, concierge service |

| Punjab National Bank | 3.00 – 3.50 | Rs. 5,000 – Rs. 10,000 | Cashback on fuel, railway ticket bookings, lifestyle benefits |

| Bank of Baroda | 3.25 – 3.75 | Rs. 5,000 – Rs. 10,000 | Free accidental insurance, rewards program, discounts |

| Canara Bank | 3.00 – 3.50 | Rs. 5,000 – Rs. 10,000 | Cashback on bill payments, health check-up benefits, rewards |

| IDFC First Bank | 3.50 – 4.00 | None | Airport lounge access, complimentary insurance, rewards |

| Union Bank of India | 3.25 – 3.75 | Rs. 5,000 – Rs. 10,000 | Cashback on groceries, fuel, and more, lifestyle privileges |

HDFC Bank

HDFC Bank boasts a variety of salary accounts, each promising attractive benefits, including interest rates. But are these rates truly the highest in the market? Let’s dive deeper and see if they live up to the hype, considering both the perks and potential drawbacks.

What HDFC Bank Offers:

- Interest Rates: Rates vary depending on the specific account type and your average monthly balance. Generally, they range from 3.00% to 4.00% p.a., which is competitive compared to other banks, but not necessarily the highest.

- Benefits: Depending on the account, you can enjoy perks like free ATM withdrawals, complimentary debit cards, discounts on various services, and even access to airport lounges.

- Network & Convenience: With a wide branch network and robust online banking platform, HDFC offers easy access and management of your finances.

ICICI Bank

ICICI Bank boasts a state-of-the-art online banking portal and mobile app, offering unparalleled convenience and efficiency. From bill payments to instant fund transfers, ICICI Bank’s digital services enable you to take care of your day-to-day banking needs effortlessly.

As we know, ICICI Bank doesn’t offer a single “one size fits all” salary account. Instead, they have various options tailored to different lifestyles and needs:

- Silver Salary Account: Ideal for starters, it offers free ATM withdrawals, online banking, and basic debit card benefits.

- Gold Salary Account: Take it up a notch with higher ATM withdrawal limits, complimentary insurance, and reward points on debit card spends.

- Titanium Salary Account: This premium option boasts airport lounge access, higher reward points, and personalized wealth management guidance.

- Defence Salary Account: Exclusively for defense personnel, it offers special benefits like complimentary insurance, higher interest rates, and discounts on army canteens.

State Bank of India (SBI)

With over 22,000 branches and 60,000+ ATMs across India, SBI ensures widespread availability and accessibility. SBI’s YONO app offers a host of features, including UPI payments, bill payments, and insurance services, making it a one-stop solution for all your banking needs.

State Bank of India (SBI), the largest public sector bank in India, offers a diverse range of salary accounts catering to various needs and preferences. In 2024, navigating these options can be tricky, so let’s break down the key features and benefits to help you choose the best fit:

Various types of salary account offered by SBI are as below:

- Basic Savings Bank Deposit (BSBD): A simple, no-frills option with no minimum balance requirement and free ATM withdrawals across SBI and other banks (limited transactions).

- Salary Savings Account: Offers free ATM withdrawals across all banks, zero balance requirements, and various other benefits like accidental death insurance and discounts on SBI services.

- Premium Salary Account: Designed for higher earners, this account boasts higher interest rates, free premium debit card with airport lounge access, and additional insurance coverage.

- State Government Salary Package (SGSP): Specially tailored for state government employees, includes zero charges for salary disbursal, free cheque issuance, and various loan benefits.

Kotak Mahindra Bank

Kotak Mahindra Bank’s 811 account offers a plethora of benefits, including cashback on bills paid, discounts on shopping, and exclusive deals on travel bookings.

Kotak Mahindra Bank’s mobile app and internet banking portal facilitate quick and efficient transactions, enhancing your banking experience.

Types of Kotak Mahindra Salary Accounts:

1. Ace Salary Account:

- Minimum Balance: Zero

- ATM Withdrawals: Free across India

- Debit Card: Platinum debit card with fuel surcharge waiver and reward points.

- Other Benefits: Personal accident death cover, lost card liability insurance, pre-approved loan offers.

2. Edge Salary Account:

- Minimum Balance: Zero

- ATM Withdrawals: Free across India

- Debit Card: Classic debit card with reward points.

- Other Benefits: Personal accident death cover, lost card liability insurance, pre-approved loan offers, access to Kotak’s digital banking platform.

3. Neo Salary Account:

- Minimum Balance: Zero

- ATM Withdrawals: Free at Kotak Mahindra Bank ATMs, charges apply elsewhere.

- Debit Card: Classic debit card with reward points.

- Other Benefits: Lost card liability insurance, access to Kotak’s digital banking platform.

4. Platina Salary Account:

- Minimum Balance: ₹10,000

- ATM Withdrawals: Free across India

- Debit Card: Platinum debit card with airport lounge access, fuel surcharge waiver, and reward points.

- Other Benefits: Personal accident death cover, lost card liability insurance, pre-approved loan offers, priority customer service.

Axis Bank

Axis Bank’s premium salary account offers exclusive benefits such as airport lounge access, complimentary movie tickets, and priority services at select branches.

Axis Bank’s mobile app and internet banking portal allow you to manage your finances efficiently, keeping pace with modern banking trends.

Types of salary accounts offered by Axis Bank are mentioned below for your reference:

- Easy Access Salary Account: Perfect for those seeking convenience and basic benefits, this account offers free ATM withdrawals, online banking, and a RuPay Platinum Debit Card.

- Liberty Salary Account: Ideal for frequent travelers, this account comes with a Liberty Debit Card offering high daily withdrawal limits, airport lounge access, and travel insurance.

- Prime Salary Account: This premium account caters to those who value exclusive perks. Enjoy higher transaction limits, a complimentary airport lounge access per quarter, and a Liberty Debit Card with dining discounts and cashback.

- Priority Salary Account: This account caters to high-net-worth individuals, offering personalized relationship management, exclusive wealth management tools, and a Priority Platinum Debit Card with premium benefits.

Punjab National Bank

In 2024, PNB offers a variety of salary accounts tailored to different needs, each with its own set of perks and features. Let’s dive in and see if one of them fits your bill:

Types of PNB Salary Accounts:

- Total Freedom Savings Account Salary: This account offers the basics: free ATM withdrawals, online banking, and mobile banking. It also earns interest on your balance, making your money work harder for you.

- High-End Salary Account: Designed for professionals with higher salaries, this account boasts higher interest rates, free accidental death insurance, and discounts on EMIs for loans taken from PNB.

- Family Protection Account: This account comes with a unique feature: free hospitalization cover for your family members. It also offers free ATM withdrawals, online banking, and mobile banking.

- PNB Junior SF Account: Ideal for parents looking to inculcate saving habits in their children, this account offers a fun and interactive experience with cartoon characters and rewards for saving.

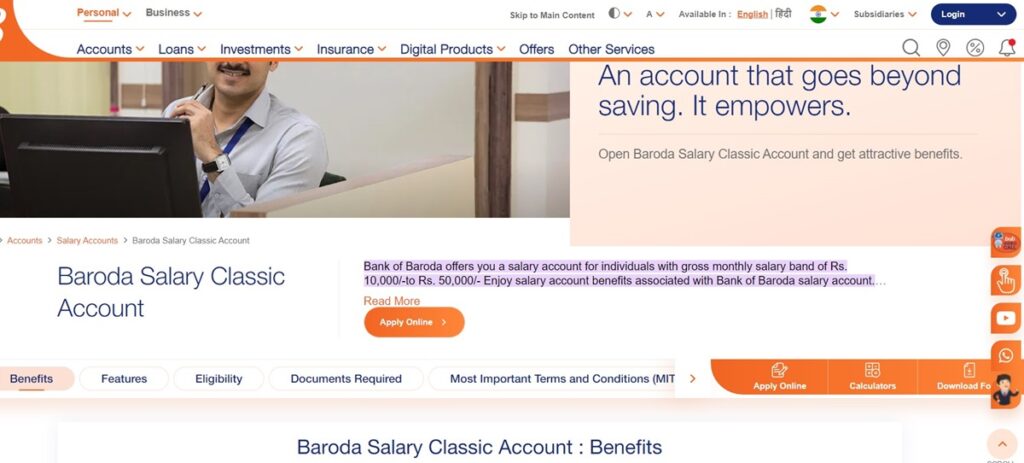

Bank of Baroda

In 2024, they’ve got several salary account options designed to cater to different needs and lifestyles. Let’s dive in and see if one might be the perfect fit for you!

Types of BoB Salary Accounts:

- Baroda Salary Classic Account: This account offers the basics with a twist! Enjoy free ATM withdrawals across India, up to 50% discount on locker rentals, and a lifetime free Rupay Platinum Debit Card. Plus, get an overdraft facility of up to ₹50,000 after three salary credits!

- Baroda Government Employee Salary Account: If you’re a government employee, this account has your name written all over it. You get free unlimited transactions (debit and credit), attractive waivers on service charges, and even personal accident cover up to ₹60 lakhs!

- Baroda Salary Plus Account: Looking for premium features? This account boasts free unlimited transactions, a complimentary Zero Balance Account for your spouse, and up to 100% discount on Demat Annual Maintenance Charges! You’ll also get a lifetime free Select/Premier Credit Card.

Canara Bank

Types of salary accounts offered by Canara Bank are mentioned below for your kind refrence:

- Variety of options: Canara Bank offers several salary account variants, like Super Savings Salary Account, Premium Payroll Package Silver, and Gold. This allows you to choose based on your needs and income bracket.

- Interest rates: Depending on the account type and your average monthly balance, you can earn interest rates ranging from 2.90% to 3.50%, which is decent in the current market.

- Wide ATM network: Canara Bank boasts a vast network of ATMs across India, making cash withdrawals convenient.

- Free accidental insurance: Some variants offer complimentary accidental death and disability insurance, providing peace of mind.

- Discounts and offers: Depending on the account type, you might enjoy discounts on movie tickets, online shopping, and bill payments.

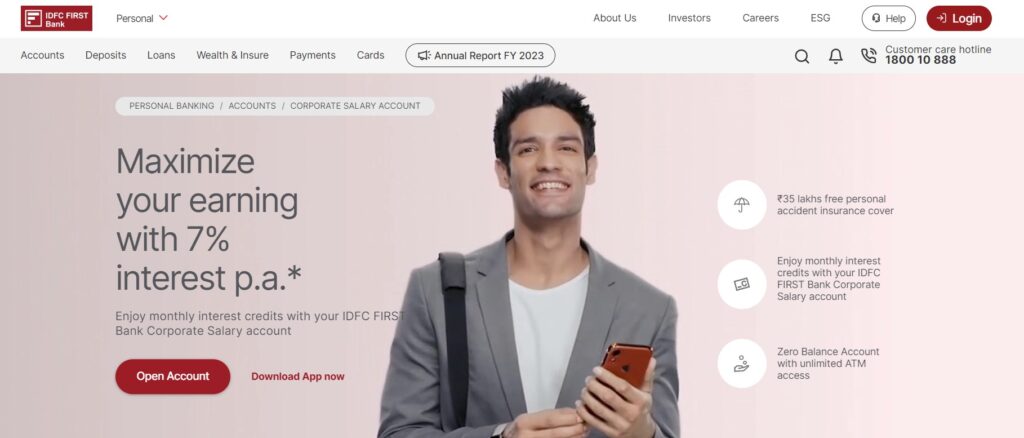

IDFC First Bank

In 2024, they’ve upped the game with their salary account offerings, promising high interest rates, zero fees, and exciting benefits.

But before you jump in, let’s dissect the details and see if it’s the perfect fit for you.

The good stuff offered by IDFC First Bank is as under:

- Zero fees: Forget about annual maintenance charges, account closure charges, and even physical ATM withdrawal fees (within India). That’s right, you can access your money freely!

- High interest rates: Earn up to 7% p.a. on your savings balance, which is significantly higher than what most traditional banks offer. This translates to real money back in your pocket!

- Multiple account options: Choose from two variants: Nation FIRST for all the basic features and Savings FIRST for additional perks like higher interest rates, debit card reward points, and complimentary insurance coverage.

- Digital convenience: Manage your account on the go with their user-friendly mobile app or internet banking platform. Say goodbye to long queues and hello to 24/7 access!

- Investment opportunities: Link your salary account to various investment options like mutual funds, bonds, and even IPOs. Grow your wealth while you manage your daily finances.

But, before finalizing this as your salary account, consider the following:

- Minimum salary requirement: You’ll need a minimum monthly salary of Rs. 18,000 to be eligible, which might not be suitable for everyone.

- Limited branch network: Compared to traditional banks, IDFC First has fewer physical branches. This might be a concern if you prefer in-person banking interactions.

- Higher minimum balance requirement for Savings FIRST: While the Nation FIRST offers zero balance, the Savings FIRST requires you to maintain a minimum average monthly balance (AMB) of Rs. 25,000.

Union Bank of India

Looking for a salary account that offers more than just a place to park your paycheck?

Union Bank of India (UBI) throws its hat in the ring with its range of salary accounts, promising convenience, rewards, and even a bit of insurance!

But is it the right fit for you in 2024? Let’s dive in and see what UBI has to offer.

UBI offers two main salary account options:

- Union Super Salary Account (USSA): This comes in two variants – USSA-I and USSA-II. Both offer free ATM withdrawals, online banking, and mobile banking access. USSA-II boasts higher interest rates and higher transaction limits, but requires a larger minimum balance.

- Union Salary Saving Account (USSA): This basic account comes with free ATM withdrawals and online banking access, but has lower interest rates and transaction limits compared to USSA-I and II.

Hangon! Here’s where things get interesting:

- Interest Rates: USSA-I and II offer tiered interest rates, meaning the more you maintain, the higher the interest you earn.

- Free Accident Insurance: Both USSA variants come with complimentary personal accident insurance, providing some peace of mind.

- Discounts and Offers: UBI partners with various merchants to offer discounts on shopping, dining, and entertainment.

- Other Benefits: Depending on the account and your employer tie-up, you might also enjoy benefits like airport lounge access, fuel surcharge waivers, and concessional interest rates on loans.

Also, before moving ahead, consider the following also:

- Minimum Balance: USSA-II requires a higher minimum balance compared to other options. Make sure you can maintain it to avoid penalty charges.

- Limited Branch Network: UBI has fewer branches compared to some other major banks. If physical branch access is important, consider this factor.

- Online Banking: While UBI offers online banking and mobile app, some users report occasional glitches or limitations.

So, finally is it a good option for you or not?

The answer depends on your needs and priorities.

If you’re looking for a basic salary account with free withdrawals and some perks, the USSA might suffice. But if you prioritize high interest rates, comprehensive insurance, and a wider branch network, you might want to explore other options.

Actionable Tips: Maximize Your Salary Account

Now that you’re armed with knowledge, let’s put it into action! Here are some practical tips to maximize the benefits of your chosen best bank for salary account in India:

- Negotiate fees: Don’t be afraid to negotiate annual charges or minimum balance requirements. Remember, you’re a valuable customer!

- Utilize all benefits: Explore all the perks offered by your salary account, from cashback offers to discounts, and leverage them to your advantage.

- Set up auto-transfers: Automate recurring expenses like rent or bill payments to avoid late fees and streamline your finances.

- Track your spending: Regularly monitor your account activity and spending patterns to identify areas where you can save money.

- Maintain a good credit score: A healthy credit score can unlock higher interest rates and better loan terms in the future.

- Opt for Direct Debits and Standing Instructions: Set up automatic payments for your utility bills, loan EMIs, and investments to avoid missing deadlines and streamline your financial transactions.

Your salary account is more than just a place to park your salary. By choosing the right bank and implementing these tips, you can transform it into a powerful tool for financial growth, convenience, and rewards.

Tips for Managing Your Salary Account

- Keep track of your expenses and savings to identify areas where you could cut costs and improve your budgeting skills.

- Set aside a portion of your monthly salary for emergency funds and long-term investments.

- Opt for auto debit facilities to avoid missing deadlines and accumulating late fees.

- Monitor your credit score regularly to maintain good standing and avail favorable interest rates on future loans.

Salary Account vs Savings Account

Here’s a grid comparing salary accounts and savings accounts:

| Feature | Salary Account | Savings Account |

|---|---|---|

| Purpose | Designed for receiving monthly salary payments. | Intended for saving and managing personal funds. |

| Monthly Credits | Regular salary credits are common. | Credits from various sources (salary, business, etc.). |

| Minimum Balance | Some banks offer zero or low minimum balance requirements. | Usually require a minimum balance to be maintained. |

| Interest Rates | Typically offer lower interest rates compared to savings accounts. | Often offer higher interest rates, especially with higher balances. |

| Withdrawal Limits | May have higher ATM withdrawal and transaction limits. | Standard ATM withdrawal and transaction limits. |

| Benefits | Often come with perks like free ATM withdrawals, debit cards, and insurance. | Benefits may include higher interest rates, overdraft facilities, and loyalty programs. |

| Accessibility | Accessible for salary credits and withdrawals. | Accessible for deposits, withdrawals, and transfers. |

| Account Closure | May require switching to a savings account upon changing jobs. | Can be closed without any specific employment conditions. |

| Purpose of Funds | Primarily used for day-to-day expenses and bill payments. | Used for long-term savings goals and emergency funds. |

Above grid provides a clear comparison between salary accounts and savings accounts, highlighting their key features and differences. This is certainly going to help you decided judiciously.

Also Read: Robert Kiyosaki 10 Keys To Financial Freedom

Saving Account Vs Current Account

Here’s a comparison grid outlining the differences between saving accounts and current accounts:

| Aspect | Saving Account | Current Account |

|---|---|---|

| Purpose | Primarily for saving money and earning interest | Mainly for conducting day-to-day financial transactions |

| Interest | Typically offers interest on deposited funds | Usually does not offer interest on deposited funds |

| Minimum Balance | Often requires maintaining a minimum balance | May or may not require a minimum balance |

| Transaction Limits | Limited number of free transactions per month | Unlimited transactions, but may incur charges |

| Overdraft Facility | Usually not available | Overdraft facility may be available for businesses |

| Usage | Suitable for individuals and small businesses | Ideal for businesses with frequent transactions |

| Fees | Minimal or no fees for basic services | Charges may apply for various transactions and services |

| Documentation | KYC documents required | KYC documents and business registration may be required |

I am quite sure that this comparison should help you understand the key differences between saving accounts and current accounts, allowing you to make an informed decision based on your financial needs and preferences.

Conclusion

Choosing the finest bank for your salary account is an important step in improving your financial situation.

By choosing a bank that meets your requirements and preferences, you can reap a slew of benefits and streamline your banking experience.

As you embark on this path, remember to stay informed, consider your options, and make proactive decisions to optimize your savings and reach your financial objectives.

With the proper salary account by your side, you may experience greater convenience, flexibility, and benefits, allowing you to take control of your funds and create a better future. Here’s to financial freedom and success!

FAQs

Can I convert my Savings Account to salary account?

Yes, you can.

If you have just changed your job, you can consider converting your Savings Account to a Salary Account.

Ensure the following to do so:

- Ensure your new employer has a banking relationship with the chosen bank.

- Visit your local bank branch and ask for the account conversion.

- Provide your new company’s details and confirm your employment status.

Keep in mind that if you haven’t received your salary in your Salary Account for three consecutive months, the account will automatically convert back to a Savings Account.

What are the benefits of salary account?

Following are some of the benefits of a salary account:

- Automatic Deposits: Salary gets automatically credited to the account, eliminating manual deposits and saving time.

- Free ATM Withdrawals: Many salary accounts offer free ATM withdrawals from the bank’s network, sometimes even other banks, reducing withdrawal fees.

- Online and Mobile Banking: Easy access to manage your account, pay bills, transfer funds, and track expenses anytime, anywhere.

- Interest Rates: Some salary accounts offer higher interest rates on your balance compared to regular savings accounts, potentially boosting your savings.

- Cashback Offers: Earn cashback on certain transactions like bill payments, online shopping, or fuel purchases, putting money back in your pocket.

- Discounts and Offers: Many banks partner with merchants to offer discounts on shopping, dining, travel, and other services.

- Insurance Coverage: Some salary accounts come with complimentary personal accident insurance, health cover, or even travel insurance, providing peace of mind.

- Investment Options: Certain banks offer access to investment products and wealth management tools directly through your salary account, helping you grow your wealth.

- Airport Lounge Access: Some high-end salary accounts offer access to airport lounges, making travel more comfortable.

- Loan Benefits: You might enjoy preferential interest rates or quicker loan processing on products like personal loans, car loans, or home loans, depending on the bank and your salary.

- Tracking Expenses: Many salary accounts offer budgeting tools and spending trackers, helping you manage your finances more effectively.

- Standing Orders and Auto-Payments: Set up automatic payments for bills and recurring expenses, ensuring timely payments and avoiding late fees.

Can I have 2 salary accounts?

Yes, you can have multiple salary accounts, allowing you to manage your finances more effectively.

Some individuals maintain multiple salary accounts by transferring funds between them monthly, ensuring smooth operations across different banks.

Having multiple salary accounts can be beneficial for various reasons, such as diversifying your banking relationships and taking advantage of specific bank benefits.

However, it’s essential to ensure that your company can credit your salary to multiple accounts if you choose this approach.

Each bank may have its policies regarding maintaining multiple salary accounts, so it’s advisable to check with your HR department or the respective banks for specific guidelines and procedures.

Can we use salary account for UPI?

Yes, you can use a salary account for UPI transactions.

UPI or Unified Payments Interface is a payment system that allows instant fund transfers between bank accounts using a mobile device.

Most salary accounts come with advanced online banking services, including UPI, allowing you to manage your finances conveniently from anywhere.

With UPI, you can transfer funds easily and quickly to other bank accounts, pay bills, and make purchases online or at physical stores.

Some salary accounts also offer additional perks like cashbacks and reward points for UPI transactions, helping you save money on your daily expenses

What is the minimum balance in HDFC salary account?

The minimum balance requirement for an HDFC salary account depends on several factors, including:

Account type: Different HDFC salary accounts have varying minimum balance requirements. Here are some common options:

- Regular Salary Account: Zero balance required.

- Salary Savings Account: Rs. 5,000 minimum balance in metro and urban areas, Rs. 2,500 in semi-urban and rural areas.

- DigiSave Youth Account: Rs. 5,000 minimum balance in metro and urban areas, Rs. 2,500 in semi-urban and rural areas.

- Premium Salary Account: Minimum balance varies depending on the variant, ranging from Rs. 10,000 to Rs. 25,000.

Location: The minimum balance requirement can differ based on whether you reside in a metropolitan, urban, semi-urban, or rural area.

Employer tie-up: In some cases, your employer might have a special agreement with HDFC that waives or lowers the minimum balance requirement for their employees.

Account age: Newly opened accounts might have a temporary minimum balance requirement for a specific period.

What happens to salary account if I leave the company?

When leaving a company, your salary account will generally be converted to a regular savings account if there are no further salary credits for three consecutive months.

During this transition period, you may wish to discuss with your new employer whether they share a banking relationship with the same bank, allowing you to retain your salary account.

Keep in mind that continuing with your existing salary account may depend on the banking arrangements between your new employer and the bank.

Alternatively, you can open a new savings account with your new employer’s preferred bank, keeping your former salary account intact if it meets your ongoing financial needs

What is premium salary account?

A premium salary account is a specialized offering by banks for high-end salary earners, providing a range of exclusive features and benefits tailored to meet the financial needs of individuals with substantial incomes.

Here are some key aspects of a premium salary account:

- Zero Balance Requirement: Premium salary accounts often come with no minimum balance stipulation, ensuring that account holders do not need to maintain a specific amount in their account.

- High-End Features: These accounts offer a host of premium features such as priority services, higher shopping limits, and personalized customer support to cater to the unique requirements of affluent customers.

- Customized Benefits: Premium salary accounts may include perks like free personal accident insurance coverage, exclusive discounts on shopping, and enhanced interest rates on savings balances.

- Priority Service: Account holders can enjoy priority banking services, faster transaction processing, and dedicated relationship managers to address their financial needs promptly.

- Additional Services: Some premium salary accounts provide specialized services to meet specific requirements, such as defense salary accounts tailored for defense personnel with unique benefits and offerings.

In essence, a premium salary account goes beyond the standard offerings of a regular salary account, providing affluent individuals with a suite of upscale benefits and personalized services to enhance their banking experience and cater to their financial aspirations.

Which bank is good for salary account?

When selecting a bank for a salary account, consider factors such as ease of setting up direct debits and electronic clearing service (ECS) mandates, privacy and security measures, terms and conditions, reviews and recommendations, and the availability of additional benefits like debit cards, access to banking services, and special offers.

Some top choices for salary accounts include:

- HDFC Bank: Known for its extensive network and competitive interest rates, HDFC Bank offers a variety of salary account options, including premium accounts with extra perks.

- ICICI Bank: ICICI Bank provides a rich payroll account for both employers and employees, featuring numerous benefits and services.

- IDFC First Bank: IDFC First Bank offers a zero-balance account with unlimited ATM access and up to ₹35 lakhs of free personal accident insurance coverage.

- Federal Bank: Featuring the Fed Salary Premium account, Federal Bank offers a zero-balance account with priority services and customized benefits.

- HSBC: HSBC offers a salary account with minimal documentation requirements and a range of digital banking solutions.

Keep in mind that the best bank for your salary account depends on your individual needs and preferences, so research and compare the options carefully before deciding.

Which is better savings or salary account?

The choice between a savings and a salary account depends on your financial habits and needs.

A savings account is ideal for long-term savings and earning interest on your balance, while a salary account is designed for receiving regular paychecks and managing day-to-day expenses.

If you prioritize saving and earning interest, a savings account may be better.

However, if you want convenience, zero balance requirements, and additional perks like free debit cards, a salary account could be more suitable.

Ultimately, the better option varies based on your financial goals and usage patterns.

For further details, refer the main body of this blogpost.

Which bank is best for TCS salary account?

Based on the feedback and preferences of individuals, HDFC Bank appears to be a popular choice for TCS salary accounts, offering digital features, good credit card history, and attractive online offers.

Additionally, ICICI Bank and Axis Bank are also preferred options for TCS salary accounts, providing a range of benefits and services.

It is advisable to consider factors such as digital features, credit card offerings, and overall banking experience when selecting the best bank for your TCS salary account. Ultimately, the decision should align with your specific financial needs and preferences.

Broadly you can consider following points to make a right decision for you:

- Interest Rates: Do you prioritize high returns on your balance? Compare interest rates offered by different banks on salary accounts.

- Fees: Are you comfortable with monthly fees or minimum balance requirements? Look for accounts with minimal charges and achievable balance requirements.

- Benefits and Perks: Are free ATM withdrawals, airport lounge access, or cashback offers important to you? Explore accounts that provide these features.

- Convenience: Do you prefer online banking, mobile app access, or extensive branch networks? Choose a bank that offers convenient banking options you’ll use.

- Customer Service: Do you value responsive and helpful customer support? Research bank ratings and reviews to consider their service quality.

- Digital Tools: Are you looking for budgeting tools, investment options, or wealth management features? Choose a bank with integrated digital tools to manage your finances comprehensively.

Can salary account be freezed by company?

No, a company cannot directly freeze your salary account, as it’s your personal account held by a bank and not under the company’s control.

However, there are few scenarios where your access to your salary account might be restricted, though not through direct freezing by the company:

- Court Order: If the company obtains a court order against you for financial reasons, like unpaid loans or misappropriation of funds, the court may freeze your bank account, including your salary account.

- 2. Garnishment: In some countries, like the US, employers can be obliged to garnish a portion of your salary for certain purposes like child support, student loans, or unpaid taxes. This means the deducted amount would be sent directly to the relevant authority, not the company, and wouldn’t technically freeze your account.

- 3. Internal Investigation: If the company suspects you of financial wrongdoing like fraud or embezzlement, they might temporarily restrict access to your company resources, including your salary account, while they conduct an internal investigation. However, this wouldn’t be a permanent freeze, and your access would be restored if the investigation clears you.

- 4. Reporting Suspicious Activity: If the company suspects your bank account activity might be linked to illegal activity, they might report it to the bank, potentially triggering account restrictions or investigations. However, this wouldn’t be directly initiated by the company.

It’s crucial to understand your employment contract and local laws to know your rights and responsibilities regarding your salary account.

If you have any concerns about potential restrictions on your account, consult a lawyer or financial advisor for specific guidance.

How do I close my salary account?

To close a salary account, you need to follow the bank’s guidelines, which may vary depending on the bank.

Generally, the process involves informing the bank of your intention to close the account and providing the necessary documentation.

Here are some general steps to follow when closing a salary account:

- Open a new bank account: Before closing your salary account, open a new bank account to ensure that you have a place to deposit your paychecks and manage your finances.

- Transfer your funds: Transfer any remaining balance in your salary account to your new account.

- Inform your bank: Contact your bank and inform them of your intention to close your salary account. They may require you to fill out a form or provide a written request.

- Provide documentation: Provide any necessary documentation, such as your ID proof, address proof, and account closure form.

- Confirm account closure: After submitting your request, confirm with your bank that your salary account has been closed.

It is crucial to remember that some banks could impose a fee for account closures, so make sure to confirm in advance with your bank. After changing employment, it’s also a good idea to keep your salary account open for a few months to make sure all deposits and payments have been made to your new account.

Can husband and wife have same salary account?

In general, it is possible for a husband and wife to have the same salary account.

However, it is more common for couples to have separate accounts to manage their finances independently or jointly.

Couples can choose to maintain joint accounts for shared expenses like household bills while also having individual accounts for personal spending.

The decision to have the same or separate salary accounts ultimately depends on the couple’s financial preferences, goals, and level of trust in managing their finances together.

Can I open salary account myself?

Yes, you can start a salary account yourself. Many banks allow you to open a salary account online or in person by providing the required papers and meeting the eligibility conditions.

Opening a salary account normally entails completing an application form, presenting evidence of identification and address, and submitting additional relevant papers.

Some banks may also mandate that a minimum amount be maintained in the account.

To choose the finest salary account that suits your financial goals and preferences, you must conduct research and comparisons of available possibilities.

Can I deposit money in my salary account?

Yes, you can deposit money in your salary account.

A salary account is a type of savings bank account that is dedicated to receiving your monthly salary deposited by your employer, but it is not bound to accept only your salary.

You can also deposit cheques and cash deposits from anyone into your salary account.

However, banks may require you to declare the source of the money if it is a large amount, and tax obligations may need to be fulfilled in some cases.

It is important to note that if you exceed the monthly number of over-the-counter transactions done for the account, it may attract a small fee.

What documents required for salary account?

To open a salary account, you typically need to provide the following documents:

- Proof of Identity: Valid government-issued photo ID such as Aadhaar card, Passport, Voter ID, or Driving License.

- Proof of Address: Documents like Aadhaar card, Passport, Voter ID, or utility bills not more than 3 months old.

- Employment Proof: A letter from your employer confirming your employment status and salary details.

- Passport Size Photographs: Usually 2-4 passport size photographs.

- PAN Card: Permanent Account Number (PAN) card for tax purposes and KYC compliance.

Having these documents ready will streamline the account opening process and ensure compliance with regulatory requirements.

It’s advisable to check with the specific bank for any additional documents they may require.

Can I deposit 5 lakhs in my salary account?

Yes, you deposit 5 lakhs in your salary account.

However, there are a few things to consider first:

- Cash Deposit Limit: Some banks may put limits on the amount of cash that can be deposited per transaction or over a given time period.

- Source of Funds: Banks are required to declare big cash deposits to the Income Tax Department (typically in excess of Rs. 10 lakh per fiscal year). If your finances are large, be prepared to explain where they came from.

- Salary Account: Some salary accounts might have restrictions on deposits not originating from your salary. Check your account terms and conditions.

- Income Tax: If the deposited amount represents income not already taxed, you might need to pay income tax on it. Consulting a tax professional is recommended for large deposits.

- Cheque Deposit: Depositing a cheque instead of cash might avoid certain limitations or reporting requirements.

- Transfer from Another Account: Transferring funds from another account electronically might be more convenient and avoid cash deposit limits.

My Social Links: Quora, Facebook, Linkedin, Pinterest, X (Twitter)